Dr. Michael Berliner, co-chairman of the Board of Directors of the Ayn Rand Institute, former professor of philosophy and executive director of the Ayn Rand Institute, reminds us of the true meaning of Independence Day.

John Adams – Declaretion of Indipendence (HD – With subtitles)

President Underwood’s Speech – House of Cards Season 3

Frank Underwood Explains Why We Watch

Kevin Spacey Explains Who Frank Underwood Is Talking To

Q8 – Trump – cut entitlements, Social Security, deficit, deliver on promises? bringing back jobs

Milton Friedman – The Free Lunch Myth

2017 – The End of Social Security?

Milton Friedman – FDR and Social Security

Milton Friedman – The Social Security Myth

Milton Friedman – The Great Depression Myth

Milton Friedman: The Rise of Socialism is Absurd

Milton Friedman – Socialism is Force

TAKE IT TO THE LIMITS: Milton Friedman on Libertarianism

Milton Friedman: The Two Major Enemies of a Free Society

Milton Friedman – The Draft – From Compulsory to Voluntary

Milton Friedman – Should Higher Education Be Subsidized?

Thomas Sowell — Dismantling America

The Difference Between Liberal and Conservative

The Passing of The Declaration of Independence – John Adams – HBO

Understanding the Declaration of Independence – 9 Key Concepts Everyone Should Know

History of the 4th of July: Crash Course US History Special

Tea, Taxes, and The American Revolution: Crash Course World History #28

4th of July Zombies – Americans Don’t Know Why We Celebrate Fourth of July!

IN CONGRESS, JULY 4, 1776

The unanimous Declarationof the thirteen unitedStates of America

hen in the Course of human events it becomes necessary for one people to dissolve the political bands which have connected them with another and to assume among the powers of the earth, the separate and equal station to which the Laws of Nature and of Nature’s God entitle them, a decent respect to the opinions of mankind requires that they should declare the causes which impel them to the separation.

We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness. — That to secure these rights, Governments are instituted among Men, deriving their just powers from the consent of the governed, — That whenever any Form of Government becomes destructive of these ends, it is the Right of the People to alter or to abolish it, and to institute new Government, laying its foundation on such principles and organizing its powers in such form, as to them shall seem most likely to effect their Safety and Happiness. Prudence, indeed, will dictate that Governments long established should not be changed for light and transient causes; and accordingly all experience hath shewn that mankind are more disposed to suffer, while evils are sufferable than to right themselves by abolishing the forms to which they are accustomed. But when a long train of abuses and usurpations, pursuing invariably the same Object evinces a design to reduce them under absolute Despotism, it is their right, it is their duty, to throw off such Government, and to provide new Guards for their future security. — Such has been the patient sufferance of these Colonies; and such is now the necessity which constrains them to alter their former Systems of Government. The history of the present King of Great Britain is a history of repeated injuries and usurpations, all having in direct object the establishment of an absolute Tyranny over these States. To prove this, let Facts be submitted to a candid world.

He has refused his Assent to Laws, the most wholesome and necessary for the public good.

He has forbidden his Governors to pass Laws of immediate and pressing importance, unless suspended in their operation till his Assent should be obtained; and when so suspended, he has utterly neglected to attend to them.

He has refused to pass other Laws for the accommodation of large districts of people, unless those people would relinquish the right of Representation in the Legislature, a right inestimable to them and formidable to tyrants only.

He has called together legislative bodies at places unusual, uncomfortable, and distant from the depository of their Public Records, for the sole purpose of fatiguing them into compliance with his measures.

He has dissolved Representative Houses repeatedly, for opposing with manly firmness his invasions on the rights of the people.

He has refused for a long time, after such dissolutions, to cause others to be elected, whereby the Legislative Powers, incapable of Annihilation, have returned to the People at large for their exercise; the State remaining in the mean time exposed to all the dangers of invasion from without, and convulsions within.

He has endeavoured to prevent the population of these States; for that purpose obstructing the Laws for Naturalization of Foreigners; refusing to pass others to encourage their migrations hither, and raising the conditions of new Appropriations of Lands.

He has obstructed the Administration of Justice by refusing his Assent to Laws for establishing Judiciary Powers.

He has made Judges dependent on his Will alone for the tenure of their offices, and the amount and payment of their salaries.

He has erected a multitude of New Offices, and sent hither swarms of Officers to harass our people and eat out their substance.

He has kept among us, in times of peace, Standing Armies without the Consent of our legislatures.

He has affected to render the Military independent of and superior to the Civil Power.

He has combined with others to subject us to a jurisdiction foreign to our constitution, and unacknowledged by our laws; giving his Assent to their Acts of pretended Legislation:

For quartering large bodies of armed troops among us:

For protecting them, by a mock Trial from punishment for any Murders which they should commit on the Inhabitants of these States:

For cutting off our Trade with all parts of the world:

For imposing Taxes on us without our Consent:

For depriving us in many cases, of the benefit of Trial by Jury:

For transporting us beyond Seas to be tried for pretended offences:

For abolishing the free System of English Laws in a neighbouring Province, establishing therein an Arbitrary government, and enlarging its Boundaries so as to render it at once an example and fit instrument for introducing the same absolute rule into these Colonies

For taking away our Charters, abolishing our most valuable Laws and altering fundamentally the Forms of our Governments:

For suspending our own Legislatures, and declaring themselves invested with power to legislate for us in all cases whatsoever.

He has abdicated Government here, by declaring us out of his Protection and waging War against us.

He has plundered our seas, ravaged our coasts, burnt our towns, and destroyed the lives of our people.

He is at this time transporting large Armies of foreign Mercenaries to compleat the works of death, desolation, and tyranny, already begun with circumstances of Cruelty & Perfidy scarcely paralleled in the most barbarous ages, and totally unworthy the Head of a civilized nation.

He has constrained our fellow Citizens taken Captive on the high Seas to bear Arms against their Country, to become the executioners of their friends and Brethren, or to fall themselves by their Hands.

He has excited domestic insurrections amongst us, and has endeavoured to bring on the inhabitants of our frontiers, the merciless Indian Savages whose known rule of warfare, is an undistinguished destruction of all ages, sexes and conditions.

In every stage of these Oppressions We have Petitioned for Redress in the most humble terms: Our repeated Petitions have been answered only by repeated injury. A Prince, whose character is thus marked by every act which may define a Tyrant, is unfit to be the ruler of a free people.

Nor have We been wanting in attentions to our British brethren. We have warned them from time to time of attempts by their legislature to extend an unwarrantable jurisdiction over us. We have reminded them of the circumstances of our emigration and settlement here. We have appealed to their native justice and magnanimity, and we have conjured them by the ties of our common kindred to disavow these usurpations, which would inevitably interrupt our connections and correspondence. They too have been deaf to the voice of justice and of consanguinity. We must, therefore, acquiesce in the necessity, which denounces our Separation, and hold them, as we hold the rest of mankind, Enemies in War, in Peace Friends.

We, therefore, the Representatives of the united States of America, in General Congress, Assembled, appealing to the Supreme Judge of the world for the rectitude of our intentions, do, in the Name, and by Authority of the good People of these Colonies, solemnly publish and declare, That these united Colonies are, and of Right ought to be Free and Independent States, that they are Absolved from all Allegiance to the British Crown, and that all political connection between them and the State of Great Britain, is and ought to be totally dissolved; and that as Free and Independent States, they have full Power to levy War, conclude Peace, contract Alliances, establish Commerce, and to do all other Acts and Things which Independent States may of right do. — And for the support of this Declaration, with a firm reliance on the protection of Divine Providence, we mutually pledge to each other our Lives, our Fortunes, and our sacred Honor.

Steve Bannon is right: Donald Trump should raise taxes on the rich

Updated by Dylan Matthews Jul 3, 2017, 12:20pm EDT

White House chief strategist Steve Bannon has a big idea that, according to Axios, he’s been pushing aggressively within the Trump administration: raising the top income tax rate. He’s reportedly telling his colleagues that the top bracket should “have a 4 in front of it.” (The current top bracket is 39.6 percent, or 43.4 after you include Medicare taxes.)

This would be a big shift for the administration. Its latest tax plan would cut the top rate on non-investment income to 35 percent, or 37.9 percent including Medicare taxes. Earlier plans featured top rates of 33 percent and 25 percent, and would lower the rate for “pass-through” income that owners of certain businesses get from 39.6 percent to a mere 15 percent, inducing a huge amount of tax evasion and cutting average rates for the rich still further.

And while Bannon has always affected a rivalry with wealthy elites, which this latest proposal fits into well, it’s doubtful that the more traditional supply-side conservatives on Trump’s economic team, namely Treasury Secretary Steve Mnuchin and National Economic Council Chair Gary Cohn, will get on board.

But they should. Trump and his team have a tremendous number of goals for tax reform. They want a dramatically lower corporate tax rate (Axios reports that Mnuchin and Cohn “aren’t bluffing when they say they want to slash the corporate tax rate to 15% from the current 35%”) and to let companies deduct all their investments immediately, instead of over time. They want a much bigger standard deduction on the individual side, and some kind of subsidy for child care.

Those are expensive changes, which require substantial pay-fors. One of the biggest that Republicans have proposed is the hugely controversial border adjustment measure, which Walmart, the Koch brothers, and other influential business lobbies are loudly opposing. Another is ending the deductibility of interest for debt, a very worthwhile proposal that is sure to enrage banks that take out massive amounts of debt; Goldman Sachs veteran Mnuchin has said he opposes this shift. On the individual side, eliminating the state and local tax deduction, as the Trump team has proposed, would raise money and reduce a big giveaway to rich people in blue states, but then again, the category “rich people in blue states” includes a lot of GOP donors as well as Trump himself.

And even if all of those controversial changes made it through, they might not be enough to pay for all the cuts that Republicans want.

Giving up on individual income tax rate cuts, and embracing higher rates for top earners, would free up a lot more money for corporate tax cuts. The Congressional Budget Office estimates that raising the brackets for people making more than $400,000 or so by 1 point each would raise about $93 billion over 10 years. For a new top rate of, say, 47 percent, that could mean as much as $650 billion over 10 years, and even more if you’re willing to hit 50 percent or raise taxes on people making under $400,000. Another option would be to do what Hillary Clinton proposed in the campaign and add a 5 percent surcharge to income above a certain threshold, without any deductions allowed; that would further reduce opportunities for tax evasion.

An even more ambitious plan, proposed by economists Alan Viard and Eric Toder and embraced by Sen. Mike Lee (R-UT), would overhaul the way the US taxes investment income. Today profits are taxed through the corporate tax code, and then again when they’re distributed to investors through dividends, or when those investors sell shares for a capital gain. Viard and Toder propose lowering the corporate rate to 15 percent and then taxing investments every year at normal income tax rates, whether or not they’re sold. That would end preferential treatment for investment income in the individual code, and let the individual tax raise quite a bit more money. It would enable a 45 or 47 percent top bracket to raise even more revenue to offset the cost of full expensing and a bigger standard deduction.

Ultimately, the Trump administration has to make a decision about what its goal in tax reform is. If the goal is to cut corporate taxes and encourage investment by companies, then Bannon is right: Top income rates should go up to pay for that. If the goal is to just funnel money to rich people, then they shouldn’t. But the former is a more defensible goal, and a top income rate of 45 or 47 percent would help get us there.

Part 2 –Story 2: Majority of American People Want and Deserve A Big, Bold, Bipartisan Tax Reform Cut — The Time Is Now For The Fair Tax Less Version of The FairTax — Trump Should Embrace Real Tax Reform By Becoming Champion of Fair Tax Less If He Wants A Booming Economy Growing At 5% Plus — No Guts — No Glory — Just Do It By Labor Day September 4, 2017 — Make America Great Again — What Good is Dreaming It If You Don’t Actually Do It! — Videos

Trump vs. OECD on tax reform

Watters visits Trump’s alma mater to talk tax reform

Rep. Meadows: Tax reform, health care and infrastructure get done by September

Speaker Ryan Guarantees That Congress Will Get Tax Reform Done In 2017

Speaker Paul Ryan Full Speech on Tax Reform 6-20-17

Ron Paul on Paul Ryan’s tax reform plan

How Trump’s tax reform plan will impact the economy

Donald Trump: Simplify the Tax Code

Donald Trump: I pay as little as possible in taxes

Grover Norquist on Speaker Ryan’s tax reform timeline

Grover Norquist: Expect dramatic tax cuts from Trump

The Pledge: Grover Norquist’s hold on the GOP

FairTax: Fire Up Our Economic Engine (Official HD)

Pence on the Fair Tax

Freedom from the IRS! – FairTax Explained in Details

Millionaire confidence plunges on Trump’s tax reform delays

What’s Up With Trump’s Tax Reform? Myths vs. Facts

The FairTax: It’s Time

Dan Mitchell explains the fair tax

Six Reasons Why the Capital Gains Tax Should Be Abolished

Is America’s Tax System Fair?

Sen. Moran Discusses FairTax Legislation on U.S. Senate Floor

Milton Friedman – Why Tax Reform Is Impossible

Milton Friedman – Is tax reform possible?

What’s Killing the American Dream?

Robert Wolf: Border adjustment not going to happen

Is Donald Trump serious about tax reform?

Sean Spicer: Trump wants to get tax reform right

Will tax reform really happen by August?

Dan Mitchell Discussing GOP Tax Plan and Corporate Rate Reduction

What Tax Reform Could Look Like Under Donald Trump | Squawk Box | CNBC

#Eakinomics – 4 Key Questions on Dynamic Scoring

What is Dynamic Scoring?

Trump Pushes ‘Major Border Tax’ to Keep Jobs in U.S.

Ryan Unexpectedly Joins Forces With Bannon on Border Tax

Kudlow: Freedom Caucus & Trump’s base is opposed to Border Adjustment Tax

Sen. Perdue: Border Adjustment Tax would “shutdown economic growth”

Sen. Tom Cotton: “I have serious concerns” w/ Border Adjustment Tax

Americans Need a Progressive Consumption Tax

Sen. Strange: “I would not” vote for a Border Adjustment Tax

CNBC: Steve Forbes on Border Adjustment Tax – “Don’t Do It” 2.8.17

Meg Whitman: Border Adjustment Tax Will Not Create Jobs | CNBC

Art Laffer: Border tax is a major mistake

Border Tax Fight Is Economists Vs. Everybody Else | Squawk Box | CNBC

Dan Mitchell Discussing GOP Tax Plan and Corporate Rate Reduction

What is a Border Adjustment?

Border Tax: What You Need to Know

Will a border adjustment tax help American businesses?

Will a border adjustment tax kill free trade?

Border adjustment tax political suicide?

Fox Pol:l 73% Want Tax Reform This Year – Cavuto

Could the border tax debate stall tax reform?

Is A Border Adjustment Tax A Good Idea?

Border Adjustment Tax: Trump’s MAGA Ace

President Donald Trump Begins First Week By Meeting With Top Business Leaders | NBC News

Dan Mitchell Fretting about GOP Border-Adjustable Tax Plan

Making Sense Of The 20 Percent Tax Proposal | Morning Joe | MSNBC

Proposed Tax Package A Dramatic Cut Even With A Border Tax?

Treasury Secretary Steve Mnuchin On Tax Reform, Growth, Border Tax, China (Full) | Squawk Box | CNBC

Wilbur Ross On Border Tax: Something Will Be Found To Fill Trillion-Dollar Hole | Squawk Box | CNBC

Honda “Impossible Dream” Commercial

Honda Advert: Impossible Dream II 2010

Lyrics

To dream the impossible dream

To fight the unbeatable foe

To bear with unbearable sorrow

To run where the brave dare not go

To right the unrightable wrong

To love pure and chaste from afar

To try when your arms are too weary

To reach the unreachable star

This is my quest, to follow that star,

No matter how hopeless, no matter how far

To fight for the right without question or cause

To be willing to march into hell for a heavenly cause

And I know if I’ll only be true to this glorious quest

That my heart will lie peaceful and calm when I’m laid to my rest

And the world will be better for this

That one man scorned and covered with scars

Still strove with his last ounce of courage

To fight the unbeatable foe, to reach the unreachable star

Donald Trump is a man who throws down gauntlets, and he threw down several big ones during his campaign for president — confronting the status quos on immigration, onhealthcare and on taxes, to name a few. He is now pursuing bold policy changes on each. But it could be Trump’s action on taxes that matters most to whether the stock market continues to ride high, GDP growth returns to a healthy 3% and, therefore, whether his presidency is judged well in posterity.

News about taxes has been relatively slow thus far in Trump’s administration. Judicial blowback against his immigration policies and Congressional blowback on healthcare reform have received far more attention than the general tax-plan principles he announced in April. Still, achieving detailed tax reform may prove even more difficult than his other policy struggles once the wheels start turning.

Before making tax reform a year-end goal, Treasury Secretary Steven Mnuchin initially said he hoped to complete tax reform by August. Senate Majority Leader Mitch McConnell reacted by saying that tax reform is a “very complicated subject” and harder to do now than the last time Congress achieved it in 1986. And passing the 1986 tax reform legislation was no easy task — it required winning the support of a Democratic House and a Republican president, and took nearly two years of intense negotiations. Alluding more cynically to the significant political obstacles that often impede changing the tax code, former House Speaker John Boehner said the passing of a tax code overhaul is “just a bunch of happy talk.”

Now, however, current Speaker Paul Ryan is also pushing for tax reform by the end of 2017, making these obstacles appear a little less daunting than if the administration were going it alone.

Aside from whether tax experts and Washington politicians are willing to upend the tax code, it is important to note where the American people stand on the need for action on taxes. It must be remembered that taxpayers may dislike the current tax system but not be convinced that Congress and the Trump administration will make it any better — change could be worse. Without a strong push from the American people, Trump’s tax reform might not materialize.

During the 2016 presidential campaign, Gallup tested several of candidate Trump’s tax proposals.

He advocated eliminating most federal income tax deductions and loopholes for the very rich, and Gallup found 63% of American adults favoring this with just 17% opposed.

His proposal to simplify the federal tax code — reducing the current seven tax brackets to four — was also popular, with 47% agreeing and only 12% disagreeing.

Trump’s plan to eliminate the estate tax paid when someone dies garnered considerably more agreement than disagreement from Americans, 54% to 19%. Notably, this is an issue that Congress and the wider public have considered in the recent past, and public sentiment on the issue today is in line with past Gallup polls on this issue, such as when it asked about keeping the estate tax from increasing in 2010.

More recently, in March 2017, Americans viewed President Trump’s general plan to “significantly cut federal income taxes for the middle class” positively: 61% agreed with the plan (with no mention of Trump in the question), 26% disagreed and 13% had no opinion. Trump’s proposal to lower corporate tax rates, however, elicited a split decision, with 38% reacting positively, 43% negatively and the potentially decisive 19% “no opinion” group apparently needing more information.

These findings suggest Americans could respond favorably to many of the specific elements of Trump’s ultimate tax plan, provided they make it into whatever legislation Congress winds up debating. For example, in spite of closing tax loopholes that favor the rich, the plan is expected to end up cutting taxes on the wealthy, not raising them. But as long as the plan also cuts taxes on the middle class, that fact alone is unlikely to sink it with Americans. Bush’s across-the-board tax cuts in 2001, which more Americans at the time said were a “good thing” than a “bad thing,” are a perfect illustration of this.

Whether Americans feel a sense of urgency about enacting tax reform is another matter.

In April 2017, Gallup found that Americans’ concern about their own federal tax burden had actually cooled somewhat, as barely half (51%) felt their taxes were “too high,” down from 57% in 2016. By contrast, in June 1985, the year before the revolutionary Tax Reform Act of 1986 went into effect, 63% of Americans said their taxes were too high.

While public demand for lowering taxes may have waned, it is not gone. Public concern about taxes fell the most over the past year among Republicans — a familiar political pattern given the partisan shift in presidential power. With a Republican in the White House, the Republican rank and file are less likely to say anything negative about the government, including about taxes. Still, 62% of Republicans call their taxes too high, as do 52% of independents and 39% of Democrats.

The implication? While not as intense as Congressional leaders may have expected, public demand for tax reform is still there, especially among the Republicans who may matter most to GOP lawmakers.

Common Ground Exists on Tax Reform

As the U.S. Congress is about to start its summer recess, tax reform remains ill defined by the administration, and negotiations over sub-issues like the border adjustment tax have stalled any pivot to immediate tax legislation. More importantly, there seems to be no bipartisan support this time, while there was under Reagan in 1986. Granted, this may seem like less of an issue now, as Republicans today control both the legislative and executive branches of the federal government. But real tax reform always makes for winners and losers, and it is problematic for only one party to pass new reforms. One need only look at the electoral consequences that Democrats have repeatedly suffered since 2010, the year they passed major healthcare reform legislation on party-line votes, to understand the danger Republicans could face if they pursue tax reform alone.

To make tax reform possible from a bipartisan standpoint, Congress needs to make sure the bill can be branded a “middle-class winner.” As noted previously, Americans favor tax cuts for the middle class, and as the following table shows, Republicans and Democrats are also more likely to believe middle-income people are currently paying too much in taxes than to say they are paying their fair share or paying too little.

Both Party Groups Tend to Believe Middle-Income Americans Pay Too Much in Federal Taxes

Republican/Lean Republican

Democrat/Lean Democratic

%

%

Too much

51

49

Fair share

40

43

Too little

5

7

No opinion

4

1

GALLUP, APRIL 5-9, 2017

To ensure tax reform enjoys at least some bipartisan support, Democrats will need a win during negotiations, meaning taxes would likely need to be raised on the nation’s wealthier class of citizens. Republicans are split on the issue of the fairness of taxes paid by upper-income people, but Democrats are in solid agreement that they pay too little.

Parties Diverge on Perceptions of What Upper-Income Americans Pay in Federal Taxes

Republican/Lean Republican

Democrat/Lean Democratic

%

%

Too much

18

4

Fair share

38

13

Too little

40

82

No opinion

4

1

GALLUP, APRIL 5-9, 2017

Bottom Line

With the Trump administration wanting tax reform before the end of 2017, Ryan is now promising to put it on the front burner. However, even Republican leaders’ enthusiasm for tax reform may not be enough to overcome the triad of legislative challenges that exist: the slimness of the Republican majorities in the U.S. House and Senate, the lack of bipartisanship in Washington and the power of special interest groups in Washington, D.C., to protect their vested interests. This is why comprehensive tax reform is historically so rare.

One thing working in Republicans’ favor is that a majority of Americans support tax relief for the middle class, and members of both major parties tend to believe middle-class taxes are too high. If the bill can be positioned strongly as middle-class tax relief, its chances for success will be higher.

At more than 73,000 pages, it’s no wonder our country’s tax code spells headache for millions of hardworking Americans across the country. This bloated document, riddled with complicated loopholes, is anything but navigable for working-class people who can’t afford to hire accountants, lawyers or tax professionals. Yet like clockwork every spring, Americans throw away countless time and treasure in an attempt to properly comply with the process of giving their hard-earned money to the federal government.

The rigors of compliance aside, our tax code penalizes economic growth and American competitiveness. By imposing some of the highest corporate tax rates in the industrialized world, American business are incentivized to entertain corporate inversions, and leave trillions of dollars of cash abroad where it can’t be invested in American growth. While the well-to-do and well-connected may be able to navigate this byzantine world, taxpayers across the country and throughout the 18 counties in Texas I represent are frustrated, and rightfully so. The American people deserve better.

Frustration with the IRS reached new levels in 2013 when revelations surfaced that the agency was targeting conservative groups. When Congress launched investigations, IRS Commissioner John Koskinen repeatedly obstructed justice by refusing to testify and failing to produce up to 24,000 emails relevant to the investigations. This is simply unacceptable.

To make matters worse, the IRS experienced a cyber-attack in 2015 that left more than 700,000 taxpayer accounts vulnerable. And according to a GAO report released just last month, the IRS has improved only marginally since that time in regard to its data security. Taxpayers should not be subject to the political whims of unelected bureaucrats who refuse to follow the law and falsify facts before Congress, all the while placing their personal financial data at risk.

As a staunch fiscal conservative, I’ve been vocal and outspoken about the need for a fairer, flatter tax code – one that doesn’t stifle growth or punish economic success. After all, Ronald Reagan famously said that the role of government should be to fostereconomic growth, not smother it. That’s why I’ve joined more than 70 of my colleagues in cosponsoring legislation that would eliminate all individual and corporate income taxes – the FairTax Act of 2015 (H.R. 25).

The FairTax Act, introduced by Rep. Rob Woodall (GA-7), eliminates all personal, corporate, gift and estate taxes and replaces them with a simple, point-of-sale consumption tax. Beyond this, it completely abolishes the IRS and all of the bureaucratic red tape and corporate cronyism that comes with it – and remains revenue neutral in the process.

The FairTax Act combats the corruption and inefficiency of the IRS, and instead promotes American growth and investment. I’m proud to be a cosponsor of this key piece of legislation, because it recognizes that more freedom and less government is the formula for economic success. It’s this model that’s allowed Texas to lead the nation in job growth since 2008, and it’s about time for Washington to get an overdue dose of these commonsense, Texas economic values. The FairTax Act will do just that, and I urge my colleagues to support it.

Congressman John Ratcliffe represents Texas’ 4th district, serving the outer eastern suburbs of the Dallas-Fort Worth Metroplexsince 2015. He is a member of the Judiciary Committee as well as the House Homeland Security Committee, serving as Chairman of its Cybersecurity, Infrastructure Protection, and Security Technologies Subcommittee. Prior to Congress, he served as Mayor of Heath, Texas. In addition, during the George W. Bush Administration, he was appointed to multiple posts, including U.S. Attorney and Chief of Anti-Terrorism and National Security for the Eastern District of Texas.

The current federal income tax system is clearly broken — unfair, overly complex, and almost impossible for most Americans to understand. But there is a reasonable, nonpartisan alternative before Congress that is both fair and easy to understand. A system that allows you to keep your whole paycheck and only pay taxes on what you spend.

The FairTax is a national sales tax that treats every person equally and allows American businesses to thrive, while generating the same tax revenue as the current four-million-word-plus tax code. Under the FairTax, every person living in the United States pays a sales tax on purchases of new goods and services, excluding necessities due to the prebate. The FairTax rate after necessities is 23% compared to combining the 15% income tax bracket with the 7.65% of employee payroll taxes under the current system — both of which will be eliminated!

Important to note: the FairTax is the only tax plan currently being proposed that includes the removal of the payroll tax.

Keep Your Paycheck

For the first time in recent history, American workers will get to keep every dime they earn; including what would have been paid in federal income taxes and payroll taxes. You will get an instant raise in your pay!

Social Security & Medicare Funding

Benefits will not change. The FairTax actually puts these programs on a more solid funding foundation. Instead of being funded by taxes on workers’ wages, which is a small pool, they’ll be funded by taxes on overall consumption by all residents. Learn More .

Get a Tax Refund in Advance on Purchases of Basic Necessities

The FairTax provides a progressive program called a prebate. This gives every legal resident household an “advance refund” at the beginning of each month so that purchases made up to the poverty level are tax-free. The prebate prevents an unfair burden on low-income families. Learn more .

Pay Tax on Only What You Spend

Be in control of your financial destiny. You alone can control your tax burden. If you’re thrifty, you’ll pay lower taxes than somebody who is not. Most importantly, you’ll be taxed fairly. Learn moreabout what is taxed.

Everyone Pays Their Fair Share

Tax evasion and the underground economy cost each taxpayer an additional $2,500 every year! But by taxing new products and services consumed, the FairTax puts everyone in the country at the same level at the cash register. Further, only legal residents are eligible for the prebate. Learn more .

The IRS is No Longer Needed

No more complicated tax forms, individual audits, or intrusive federal bureaucracy. Retailers will collect the FairTax just as they do now with state sales taxes. All money will be collected and remitted to the U.S. Treasury, and both the retailers and states will be paid a fee for their collection service. Learn More

Summer looms with GOP stuck on health care, budget, taxes

By The Associated Press

June 30, 2017 4:45 pm

The Capitol in Washington is quiet after lawmakers departed the for the Independence Day recess, Friday, June 30, 2017. The Republican leadership in the Senate decided this week to delay a vote on their…

WASHINGTON (AP) — Republicans are stuck on health care, can’t pass a budget, and hopes for a big, bipartisan infrastructure package are fizzling. Overhauling the tax code looks more and more like a distant dream.

The GOP-led Congress has yet to salt away a single major legislative accomplishment for President Donald Trump — and a summer of drift may lead to a logistical nightmare this fall.

Instead, Trump’s allies appear both divided and indecisive, unable to deliver on his agenda while letting other must-do congressional business — chiefly their core responsibilities of passing a budget and spending bills, and keeping the government solvent — slide onto an already daunting fall agenda that is looking more and more like it’ll be a train wreck.

Friday brought more bad news for Speaker Paul Ryan, R-Wis., and other House leaders as 20 GOP moderates signaled a revolt on the budget, penning a letter to Ryan announcing their opposition to an emerging plan to force cuts to government agencies and benefit programs such as food stamps. The letter, authored by Rep. Charlie Dent, R-Pa., warned that without an agreement with Democrats on increasing agency spending, moderates will be “reticent to support any budget.”

“It’s looking like they’re very disorganized. They got obviously a lot of conflict over spending preferences and it’s not just a two-way conflict,” said top House Budget Committee Democrat John Yarmuth of Kentucky. “It’s just a tough Rubik’s Cube they’re trying to solve.”

So it’s not just the Senate effort to repeal and replace Democrat Barack Obama’s health care law that’s foundering. The annual congressional budget measure — a prerequisite to this fall’s hoped-for tax effort — is languishing as well, as are the 12 annual spending bills that typically consume weeks of House floor time each summer.

But GOP leaders say all is going well. Ryan told a Wisconsin radio host on Thursday that “it’s the most productive Congress since the mid-’80s” and issued a news release Friday titled “Despite What You May Hear, We Are Getting Things Done.” The release cites a bipartisan Department of Veterans Affairs accountability measure and 14 bills repealing Obama-era regulations as Congress’ top achievements.

“It would be hard to fault the average American for thinking all that’s going on in Washington these days is high-drama hearings and partisan sniping,” Ryan said. “But amid the countdown clocks and cable news chatter, something important is happening: Congress is getting things done to help improve people’s lives.”

In the first year of a presidency, the annual August congressional recess is a traditional point to take stock. By that point, Obama had signed an economic recovery bill and President George W. Bush had won his landmark tax cuts, while President Bill Clinton was celebrating a hard-fought budget package.

Trump has no comparable successes to trumpet — but his allies in Congress say they’re not worried.

“We laid out an agenda in November and December, and we’re needing to get there,” said House Rules Committee Chairman Pete Sessions, R-Texas. “And we can effectively get there. The questions that confound us are those that we can answer ourselves. And we will.”

And as Republicans are stalled on health care, the budget and infrastructure, there are several other problems that need to be taken care of, including increasing the nation’s borrowing authority, preventing a government shutdown, and lifting budget “caps” that are hobbling efforts to beef up the military.

Unlike health care, the debt limit and a deal to fix the spending caps — a leftover from a failed 2011 budget deal — can only be resolved with Democratic help. However, they promise to consume political capital and valuable time and energy, and there’s no political pay-off, other than forestalling disaster.

First, Congress is off on vacation to return in July for a three-week session. Then comes the traditional monthlong August recess.

After Labor Day comes a four-week sprint to October and the deadline to avert a government shutdown with a temporary spending bill — and to forestall a disastrous default on U.S. obligations by lifting the debt limit, which is a politically toxic vote for many Republicans.

Sentiment is building among some lawmakers to shorten the recess to make progress on the unfinished work that is piling up. On Friday, 10 GOP senators, led by David Perdue of Georgia, sent Majority Leader Mitch McConnell, R-Ky., a letter citing delays on health care, the budget, a stopgap spending bill and the debt limit as reasons to consider canceling some or all of the recess.

“If we successfully navigate those priorities, we can finally get to our once in a generation opportunity on tax reform,” the letter said. “Growing the economy, repairing our infrastructure, and rebuilding our military are all dependent on accomplishing the tasks before us.”

High-income Americans pay most income taxes, but enough to be ‘fair’?

BY DREW DESILVER

Tax-deadline season isn’t many people’s favorite time of the year, but most Americans are OK with the amount of tax they pay. It’s what other people pay, or don’t pay, that bothers them.

Just over half (54%) of Americans surveyed in fall by Pew Research Center said they pay about the right amount in taxes considering what they get from the federal government, versus 40% who said they pay more than their fair share. But in a separate 2015 surveyby the Center, some six-in-ten Americans said they were bothered a lot by the feeling that “some wealthy people” and “some corporations” don’t pay their fair share.

It’s true that corporations are funding a smaller share of overall government operations than they used to. In fiscal 2015, the federal government collected $343.8 billion from corporate income taxes, or 10.6% of its total revenue. Back in the 1950s, corporate income tax generated between a quarter and a third of federal revenues (though payroll taxes have grown considerably over that period).

Nor have corporate tax receipts kept pace with the overall growth of the U.S. economy. Inflation-adjusted gross domestic product has risen 153% since 1980, while inflation-adjusted corporate tax receipts were 115% higher in fiscal 2015 than in fiscal 1980, according to the Bureau of Economic Analysis. There have been a lot of ups and downs over that period, as corporate tax receipts tend to rise during expansions and drop off in recessions. In fiscal 2007, for instance, corporate taxes hit $370.2 billion (in current dollars), only to plunge to $138.2 billion in 2009 as businesses felt the impact of the Great Recession.

Corporations also employ battalions of tax lawyers to find ways to reduce their tax bills, from running income through subsidiaries in low-tax foreign countries to moving overseas entirely, in what’s known as a corporate inversion (a practice the Treasury Department has moved to discourage).

But in Tax Land, the line between corporations and people can be fuzzy. While most major corporations (“C corporations” in tax lingo) pay according to the corporate tax laws, many other kinds of businesses – sole proprietorships, partnerships and closely held “S corporations” – fall under the individual income tax code, because their profits and losses are passed through to individuals. And by design, wealthier Americans pay most of the nation’s total individual income taxes.

In 2014, people with adjusted gross income, or AGI, above $250,000 paid just over half (51.6%) of all individual income taxes, though they accounted for only 2.7% of all returns filed, according to our analysis of preliminary IRS data. Their average tax rate (total taxes paid divided by cumulative AGI) was 25.7%. By contrast, people with incomes of less than $50,000 accounted for 62.3% of all individual returns filed, but they paid just 5.7% of total taxes. Their average tax rate was 4.3%.

The relative tax burdens borne by different income groups changes over time, due both to economic conditions and the constantly shifting provisions of tax law. For example, using more comprehensive IRS data covering tax years 2000 through 2011, we found that people who made between $100,000 and $200,000 paid 23.8% of the total tax liability in 2011, up from 18.8% in 2000. Filers in the $50,000-to-$75,000 group, on the other hand, paid 12% of the total liability in 2000 but only 9.1% in 2011. (The tax liability figures include a few taxes, such as self-employment tax and the “nanny tax,” that people typically pay along with their income taxes.)

All told, individual income taxes accounted for a little less than half (47.4%) of government revenue, a share that’s been roughly constant since World War II. The federal government collected $1.54 trillion from individual income taxes in fiscal 2015, making it the national government’s single-biggest revenue source. (Other sources of federal revenue include corporate income taxes, the payroll taxes that fund Social Security and Medicare, excise taxes such as those on gasoline and cigarettes, estate taxes, customs duties and payments from the Federal Reserve.) Until the 1940s, when the income tax was expanded to help fund the war effort, generally only the very wealthy paid it.

Since the 1970s, the segment of federal revenues that has grown the most is the payroll tax – those line items on your pay stub that go to pay for Social Security and Medicare. For most people, in fact, payroll taxes take a bigger bite out of their paycheck than federal income tax. Why? The 6.2% Social Security withholding tax only applies to wages up to $118,500. For example, a worker earning $40,000 will pay $2,480 (6.2%) in Social Security tax, but an executive earning $400,000 will pay $7,347 (6.2% of $118,500), for an effective rate of just 1.8%. By contrast, the 1.45% Medicare tax has no upper limit, and in fact high earners pay an extra 0.9%.

All but the top-earning 20% of American families pay more in payroll taxes than in federal income taxes, according to a Treasury Department analysis.

Still, that analysis confirms that, after all federal taxes are factored in, the U.S. tax system as a whole is progressive. The top 0.1% of families pay the equivalent of 39.2% and the bottom 20% have negative tax rates (that is, they get more money back from the government in the form of refundable tax credits than they pay in taxes).

Of course, people can and will differ on whether any of this constitutes a “fair” tax system. Depending on their politics and personal situations, some would argue for a more steeply progressive structure, others for a flatter one. Finding the right balance can be challenging to the point of impossibility: As Jean-Baptiste Colbert, Louis XIV’s finance minister, is said to have remarked: “The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing.”

Note: This is an update of an earlier post published March 24, 2015.

Summary of the Latest Federal Income Tax Data, 2016 Update

February 1, 2017

Scott Greenberg

The Internal Revenue Service has recently released new data on individual income taxes for calendar year 2014, showing the number of taxpayers, adjusted gross income, and income tax shares by income percentiles.[1]

The data demonstrates that the U.S. individual income tax continues to be very progressive, borne mainly by the highest income earners.

In 2014, 139.6 million taxpayers reported earning $9.71 trillion in adjusted gross income and paid $1.37 trillion in individual income taxes.

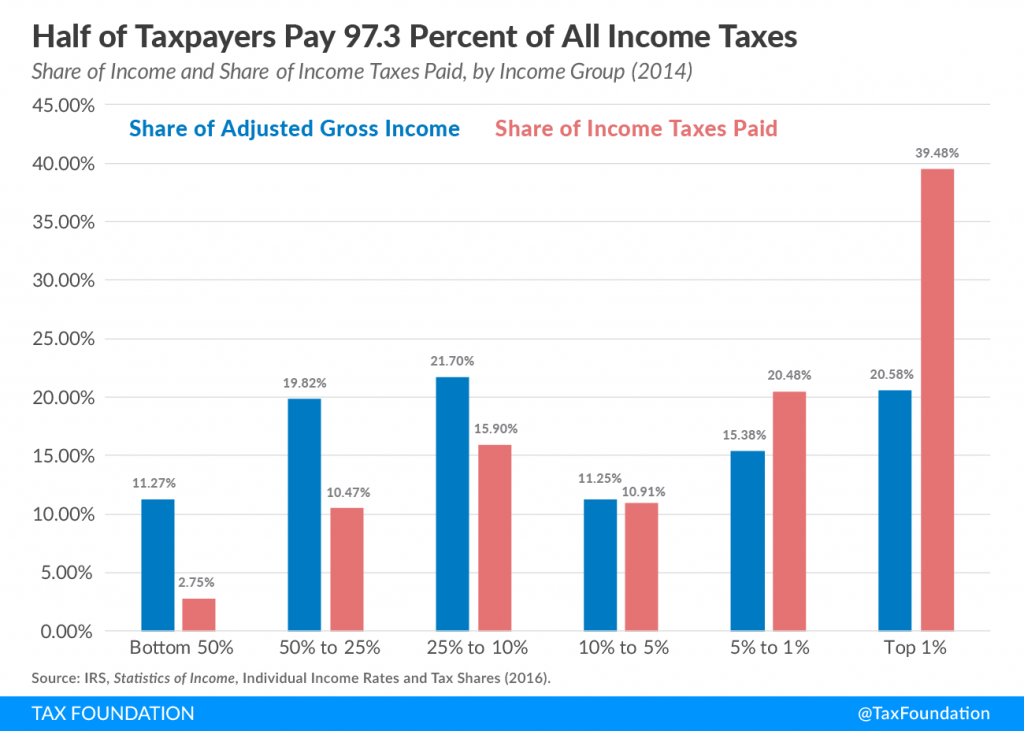

The share of income earned by the top 1 percent of taxpayers rose to 20.6 percent in 2014. Their share of federal individual income taxes also rose, to 39.5 percent.

In 2014, the top 50 percent of all taxpayers paid 97.3 percent of all individual income taxes while the bottom 50 percent paid the remaining 2.7 percent.

The top 1 percent paid a greater share of individual income taxes (39.5 percent) than the bottom 90 percent combined (29.1 percent).

The top 1 percent of taxpayers paid a 27.1 percent individual income tax rate, which is more than seven times higher than taxpayers in the bottom 50 percent (3.5 percent).

Reported Income and Taxes Paid Both Increased Significantly in 2014

Taxpayers reported $9.71 trillion in adjusted gross income (AGI) on 139.5 million tax returns in 2014. Total AGI grew by $675 billion from the previous year’s levels. There were 1.2 million more returns filed in 2014 than in 2013, meaning that average AGI rose by $4,252 per return, or 6.5 percent.

Meanwhile, taxpayers paid $1.37 trillion in individual income taxes in 2014, an 11.5 percent increase from taxes paid in the previous year. The average individual income tax rate for all taxpayers rose from 13.64 percent to 14.16 percent. Moreover, the average tax rate increased for all income groups, except for the top 0.1 percent of taxpayers, whose average rate decreased from 27.91 percent to 27.67 percent.

The most likely explanation behind the higher tax rates in 2014 is a phenomenon known as “real bracket creep.” [2] As incomes rise, households are pushed into higher tax brackets, and are subject to higher overall tax rates on their income. On the other hand, the likely reason why the top 0.1 percent of households saw a slightly lower tax rate in 2014 is because a higher portion of their income consisted of long-term capital gains, which are subject to lower tax rates.[3]

The share of income earned by the top 1 percent rose to 20.58 percent of total AGI, up from 19.04 percent in 2013. The share of the income tax burden for the top 1 percent also rose, from 37.80 percent in 2013 to 39.48 percent in 2014.

Top 1%

Top 5%

Top 10%

Top 25%

Top 50%

Bottom 50%

All Taxpayers

Table 1. Summary of Federal Income Tax Data, 2014

Number of Returns

1,395,620

6,978,102

13,956,203

34,890,509

69,781,017

69,781,017

139,562,034

Adjusted Gross Income ($ millions)

$1,997,819

$3,490,867

$4,583,416

$6,690,287

$8,614,544

$1,094,119

$9,708,663

Share of Total Adjusted Gross Income

20.58%

35.96%

47.21%

68.91%

88.73%

11.27%

100.00%

Income Taxes Paid ($ millions)

$542,640

$824,153

$974,124

$1,192,679

$1,336,637

$37,740

$1,374,379

Share of Total Income Taxes Paid

39.48%

59.97%

70.88%

86.78%

97.25%

2.75%

100.00%

Income Split Point

$465,626

$188,996

$133,445

$77,714

$38,173

Average Tax Rate

27.16%

23.61%

21.25%

17.83%

15.52%

3.45%

14.16%

Note: Does not include dependent filers

High-Income Americans Paid the Majority of Federal Taxes

In 2014, the bottom 50 percent of taxpayers (those with AGIs below $38,173) earned 11.27 percent of total AGI. This group of taxpayers paid approximately $38 billion in taxes, or 2.75 percent of all income taxes in 2014.

In contrast, the top 1 percent of all taxpayers (taxpayers with AGIs of $465,626 and above) earned 20.58 percent of all AGI in 2014, but paid 39.48 percent of all federal income taxes.

In 2014, the top 1 percent of taxpayers accounted for more income taxes paid than the bottom 90 percent combined. The top 1 percent of taxpayers paid $543 billion, or 39.48 percent of all income taxes, while the bottom 90 percent paid $400 billion, or 29.12 percent of all income taxes.

Figure 1.

High-Income Taxpayers Pay the Highest Average Tax Rates

The 2014 IRS data shows that taxpayers with higher incomes pay much higher average individual income tax rates than lower-income taxpayers.[4]

The bottom 50 percent of taxpayers (taxpayers with AGIs below $38,173) faced an average income tax rate of 3.45 percent. As household income increases, the IRS data shows that average income tax rates rise. For example, taxpayers with AGIs between the 10th and 5th percentile ($133,445 and $188,996) pay an average rate of 13.7 percent – almost four times the rate paid by those in the bottom 50 percent.

The top 1 percent of taxpayers (AGI of $465,626 and above) paid the highest effective income tax rate, at 27.2 percent, 7.9 times the rate faced by the bottom 50 percent of taxpayers.

Figure 2.

Taxpayers at the very top of the income distribution, the top 0.1 percent (with AGIs over $2.14 million), paid an even higher average tax rate, of 27.7 percent.

Appendix

Year

Total

Top 0.1%

Top 1%

Top

5%

Between

5% & 10%

Top 10%

Between 10% & 25%

Top 25%

Between 25% & 50%

Top 50%

Bottom 50%

Table 2. Number of Federal Individual Income Tax Returns Filed 1980–2014 (Thousands)

Source: Internal Revenue Service.

1980

93,239

932

4,662

4,662

9,324

13,986

23,310

23,310

46,619

46,619

1981

94,587

946

4,729

4,729

9,459

14,188

23,647

23,647

47,293

47,293

1982

94,426

944

4,721

4,721

9,443

14,164

23,607

23,607

47,213

47,213

1983

95,331

953

4,767

4,767

9,533

14,300

23,833

23,833

47,665

47,665

1984

98,436

984

4,922

4,922

9,844

14,765

24,609

24,609

49,218

49,219

1985

100,625

1,006

5,031

5,031

10,063

15,094

25,156

25,156

50,313

50,313

1986

102,088

1,021

5,104

5,104

10,209

15,313

25,522

25,522

51,044

51,044

The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line not strictly comparable

1987

106,155

1,062

5,308

5,308

10,615

15,923

26,539

26,539

53,077

53,077

1988

108,873

1,089

5,444

5,444

10,887

16,331

27,218

27,218

54,436

54,436

1989

111,313

1,113

5,566

5,566

11,131

16,697

27,828

27,828

55,656

55,656

1990

112,812

1,128

5,641

5,641

11,281

16,922

28,203

28,203

56,406

56,406

1991

113,804

1,138

5,690

5,690

11,380

17,071

28,451

28,451

56,902

56,902

1992

112,653

1,127

5,633

5,633

11,265

16,898

28,163

28,163

56,326

56,326

1993

113,681

1,137

5,684

5,684

11,368

17,052

28,420

28,420

56,841

56,841

1994

114,990

1,150

5,749

5,749

11,499

17,248

28,747

28,747

57,495

57,495

1995

117,274

1,173

5,864

5,864

11,727

17,591

29,319

29,319

58,637

58,637

1996

119,442

1,194

5,972

5,972

11,944

17,916

29,860

29,860

59,721

59,721

1997

121,503

1,215

6,075

6,075

12,150

18,225

30,376

30,376

60,752

60,752

1998

123,776

1,238

6,189

6,189

12,378

18,566

30,944

30,944

61,888

61,888

1999

126,009

1,260

6,300

6,300

12,601

18,901

31,502

31,502

63,004

63,004

2000

128,227

1,282

6,411

6,411

12,823

19,234

32,057

32,057

64,114

64,114

The IRS changed methodology, so data above and below this line not strictly comparable

2001

119,371

119

1,194

5,969

5,969

11,937

17,906

29,843

29,843

59,685

59,685

2002

119,851

120

1,199

5,993

5,993

11,985

17,978

29,963

29,963

59,925

59,925

2003

120,759

121

1,208

6,038

6,038

12,076

18,114

30,190

30,190

60,379

60,379

2004

122,510

123

1,225

6,125

6,125

12,251

18,376

30,627

30,627

61,255

61,255

2005

124,673

125

1,247

6,234

6,234

12,467

18,701

31,168

31,168

62,337

62,337

2006

128,441

128

1,284

6,422

6,422

12,844

19,266

32,110

32,110

64,221

64,221

2007

132,655

133

1,327

6,633

6,633

13,265

19,898

33,164

33,164

66,327

66,327

2008

132,892

133

1,329

6,645

6,645

13,289

19,934

33,223

33,223

66,446

66,446

2009

132,620

133

1,326

6,631

6,631

13,262

19,893

33,155

33,155

66,310

66,310

2010

135,033

135

1,350

6,752

6,752

13,503

20,255

33,758

33,758

67,517

67,517

2011

136,586

137

1,366

6,829

6,829

13,659

20,488

34,146

34,146

68,293

68,293

2012

136,080

136

1,361

6,804

6,804

13,608

20,412

34,020

34,020

68,040

68,040

2013

138,313

138

1,383

6,916

6,916

13,831

20,747

34,578

34,578

69,157

69,157

2014

139,562

140

1,396

6,978

6,978

13,956

20,934

34,891

34,891

69,781

69,781

Year

Total

Top 0.1%

Top 1%

Top 5%

Between 5% & 10%

Top 10%

Between 10% & 25%

Top 25%

Between 25% & 50%

Top 50%

Bottom 50%

Table 3. Adjusted Gross Income of Taxpayers in Various Income Brackets, 1980–2014 ($Billions)

Source: Internal Revenue Service.

1980

$1,627

$138

$342

$181

$523

$400

$922

$417

$1,339

$288

1981

$1,791

$149

$372

$201

$573

$442

$1,015

$458

$1,473

$318

1982

$1,876

$167

$398

$207

$605

$460

$1,065

$478

$1,544

$332

1983

$1,970

$183

$428

$217

$646

$481

$1,127

$498

$1,625

$344

1984

$2,173

$210

$482

$240

$723

$528

$1,251

$543

$1,794

$379

1985

$2,344

$235

$531

$260

$791

$567

$1,359

$580

$1,939

$405

1986

$2,524

$285

$608

$278

$887

$604

$1,490

$613

$2,104

$421

The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line not strictly comparable

1987

$2,814

$347

$722

$316

$1,038

$671

$1,709

$664

$2,374

$440

1988

$3,124

$474

$891

$342

$1,233

$718

$1,951

$707

$2,658

$466

1989

$3,299

$468

$918

$368

$1,287

$768

$2,054

$751

$2,805

$494

1990

$3,451

$483

$953

$385

$1,338

$806

$2,144

$788

$2,933

$519

1991

$3,516

$457

$943

$400

$1,343

$832

$2,175

$809

$2,984

$532

1992

$3,681

$524

$1,031

$413

$1,444

$856

$2,299

$832

$3,131

$549

1993

$3,776

$521

$1,048

$426

$1,474

$883

$2,358

$854

$3,212

$563

1994

$3,961

$547

$1,103

$449

$1,552

$929

$2,481

$890

$3,371

$590

1995

$4,245

$620

$1,223

$482

$1,705

$985

$2,690

$938

$3,628

$617

1996

$4,591

$737

$1,394

$515

$1,909

$1,043

$2,953

$992

$3,944

$646

1997

$5,023

$873

$1,597

$554

$2,151

$1,116

$3,268

$1,060

$4,328

$695

1998

$5,469

$1,010

$1,797

$597

$2,394

$1,196

$3,590

$1,132

$4,721

$748

1999

$5,909

$1,153

$2,012

$641

$2,653

$1,274

$3,927

$1,199

$5,126

$783

2000

$6,424

$1,337

$2,267

$688

$2,955

$1,358

$4,314

$1,276

$5,590

$834

The IRS changed methodology, so data above and below this line not strictly comparable

2001

$6,116

$492

$1,065

$1,934

$666

$2,600

$1,334

$3,933

$1,302

$5,235

$881

2002

$5,982

$421

$960

$1,812

$660

$2,472

$1,339

$3,812

$1,303

$5,115

$867

2003

$6,157

$466

$1,030

$1,908

$679

$2,587

$1,375

$3,962

$1,325

$5,287

$870

2004

$6,735

$615

$1,279

$2,243

$725

$2,968

$1,455

$4,423

$1,403

$5,826

$908

2005

$7,366

$784

$1,561

$2,623

$778

$3,401

$1,540

$4,940

$1,473

$6,413

$953

2006

$7,970

$895

$1,761

$2,918

$841

$3,760

$1,652

$5,412

$1,568

$6,980

$990

2007

$8,622

$1,030

$1,971

$3,223

$905

$4,128

$1,770

$5,898

$1,673

$7,571

$1,051

2008

$8,206

$826

$1,657

$2,868

$905

$3,773

$1,782

$5,555

$1,673

$7,228

$978

2009

$7,579

$602

$1,305

$2,439

$878

$3,317

$1,740

$5,058

$1,620

$6,678

$900

2010

$8,040

$743

$1,517

$2,716

$915

$3,631

$1,800

$5,431

$1,665

$7,096

$944

2011

$8,317

$737

$1,556

$2,819

$956

$3,775

$1,866

$5,641

$1,716

$7,357

$961

2012

$9,042

$1,017

$1,977

$3,331

$997

$4,328

$1,934

$6,262

$1,776

$8,038

$1,004

2013

$9,034

$816

$1,720

$3,109

$1,034

$4,143

$2,008

$6,152

$1,844

$7,996

$1,038

2014

$9,709

$986

$1,998

$3,491

$1,093

$4,583

$2,107

$6,690

$1,924

$8,615

$1,094

Year

Total

Top 0.1%

Top 1%

Top 5%

Between 5% & 10%

Top 10%

Between 10% & 25%

Top 25%

Between 25% & 50%

Top 50%

Bottom 50%

Table 4. Total Income Tax after Credits, 1980–2014 ($Billions)

Source: Internal Revenue Service.

1980

$249

$47

$92

$31

$123

$59

$182

$50

$232

$18

1981

$282

$50

$99

$36

$135

$69

$204

$57

$261

$21

1982

$276

$53

$100

$34

$134

$66

$200

$56

$256

$20

1983

$272

$55

$101

$34

$135

$64

$199

$54

$252

$19

1984

$297

$63

$113

$37

$150

$68

$219

$57

$276

$22

1985

$322

$70

$125

$41

$166

$73

$238

$60

$299

$23

1986

$367

$94

$156

$44

$201

$78

$279

$64

$343

$24

The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line not strictly comparable

1987

$369

$92

$160

$46

$205

$79

$284

$63

$347

$22

1988

$413

$114

$188

$48

$236

$85

$321

$68

$389

$24

1989

$433

$109

$190

$51

$241

$93

$334

$73

$408

$25

1990

$447

$112

$195

$52

$248

$97

$344

$77

$421

$26

1991

$448

$111

$194

$56

$250

$96

$347

$77

$424

$25

1992

$476

$131

$218

$58

$276

$97

$374

$78

$452

$24

1993

$503

$146

$238

$60

$298

$101

$399

$80

$479

$24

1994

$535

$154

$254

$64

$318

$108

$425

$84

$509

$25

1995

$588

$178

$288

$70

$357

$115

$473

$88

$561

$27

1996

$658

$213

$335

$76

$411

$124

$535

$95

$630

$28

1997

$727

$241

$377

$82

$460

$134

$594

$102

$696

$31

1998

$788

$274

$425

$88

$513

$139

$652

$103

$755

$33

1999

$877

$317

$486

$97

$583

$150

$733

$109

$842

$35

2000

$981

$367

$554

$106

$660

$164

$824

$118

$942

$38

The IRS changed methodology, so data above and below this line not strictly comparable

2001

$885

$139

$294

$462

$101

$564

$158

$722

$120

$842

$43

2002

$794

$120

$263

$420

$93

$513

$143

$657

$104

$761

$33

2003

$746

$115

$251

$399

$85

$484

$133

$617

$98

$715

$30

2004

$829

$142

$301

$467

$91

$558

$137

$695

$102

$797

$32

2005

$932

$176

$361

$549

$98

$647

$145

$793

$106

$898

$33

2006

$1,020

$196

$402

$607

$108

$715

$157

$872

$113

$986

$35

2007

$1,112

$221

$443

$666

$117

$783

$170

$953

$122

$1,075

$37

2008

$1,029

$187

$386

$597

$115

$712

$168

$880

$117

$997

$32

2009

$863

$146

$314

$502

$101

$604

$146

$749

$93

$842

$21

2010

$949

$170

$355

$561

$110

$670

$156

$827

$100

$927

$22

2011

$1,043

$168

$366

$589

$123

$712

$181

$893

$120

$1,012

$30

2012

$1,185

$220

$451

$699

$133

$831

$193

$1,024

$128

$1,152

$33

2013

$1,232

$228

$466

$721

$139

$860

$203

$1,063

$135

$1,198

$34

2014

$1,374

$273

$543

$824

$150

$974

$219

$1,193

$144

$1,337

$38

Year

Total

Top 0.1%

Top 1%

Top 5%

Between 5% & 10%

Top 10%

Between 10% & 25%

Top 25%

Between 25% & 50%

Top 50%

Bottom 50%

Table 5. Adjusted Gross Income Shares, 1980–2014 (percent of total AGI earned by each group)

Source: Internal Revenue Service.

1980

100%

8.46%

21.01%

11.12%

32.13%

24.57%

56.70%

25.62%

82.32%

17.68%

1981

100%

8.30%

20.78%

11.20%

31.98%

24.69%

56.67%

25.59%

82.25%

17.75%

1982

100%

8.91%

21.23%

11.03%

32.26%

24.53%

56.79%

25.50%

82.29%

17.71%

1983

100%

9.29%

21.74%

11.04%

32.78%

24.44%

57.22%

25.30%

82.52%

17.48%

1984

100%

9.66%

22.19%

11.06%

33.25%

24.31%

57.56%

25.00%

82.56%

17.44%

1985

100%

10.03%

22.67%

11.10%

33.77%

24.21%

57.97%

24.77%

82.74%

17.26%

1986

100%

11.30%

24.11%

11.02%

35.12%

23.92%

59.04%

24.30%

83.34%

16.66%

The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line not strictly comparable

1987

100%

12.32%

25.67%

11.23%

36.90%

23.85%

60.75%

23.62%

84.37%

15.63%

1988

100%

15.16%

28.51%

10.94%

39.45%

22.99%

62.44%

22.63%

85.07%

14.93%

1989

100%

14.19%

27.84%

11.16%

39.00%

23.28%

62.28%

22.76%

85.04%

14.96%

1990

100%

14.00%

27.62%

11.15%

38.77%

23.36%

62.13%

22.84%

84.97%

15.03%

1991

100%

12.99%

26.83%

11.37%

38.20%

23.65%

61.85%

23.01%

84.87%

15.13%

1992

100%

14.23%

28.01%

11.21%

39.23%

23.25%

62.47%

22.61%

85.08%

14.92%

1993

100%

13.79%

27.76%

11.29%

39.05%

23.40%

62.45%

22.63%

85.08%

14.92%

1994

100%

13.80%

27.85%

11.34%

39.19%

23.45%

62.64%

22.48%

85.11%

14.89%

1995

100%

14.60%

28.81%

11.35%

40.16%

23.21%

63.37%

22.09%

85.46%

14.54%

1996

100%

16.04%

30.36%

11.23%

41.59%

22.73%

64.32%

21.60%

85.92%

14.08%

1997

100%

17.38%

31.79%

11.03%

42.83%

22.22%

65.05%

21.11%

86.16%

13.84%

1998

100%

18.47%

32.85%

10.92%

43.77%

21.87%

65.63%

20.69%

86.33%

13.67%

1999

100%

19.51%

34.04%

10.85%

44.89%

21.57%

66.46%

20.29%

86.75%

13.25%

2000

100%

20.81%

35.30%

10.71%

46.01%

21.15%

67.15%

19.86%

87.01%

12.99%

The IRS changed methodology, so data above and below this line not strictly comparable

2001

100%

8.05%

17.41%

31.61%

10.89%

42.50%

21.80%

64.31%

21.29%

85.60%

14.40%

2002

100%

7.04%

16.05%

30.29%

11.04%

41.33%

22.39%

63.71%

21.79%

85.50%

14.50%

2003

100%

7.56%

16.73%

30.99%

11.03%

42.01%

22.33%

64.34%

21.52%

85.87%

14.13%

2004

100%

9.14%

18.99%

33.31%

10.77%

44.07%

21.60%

65.68%

20.83%

86.51%

13.49%

2005

100%

10.64%

21.19%

35.61%

10.56%

46.17%

20.90%

67.07%

19.99%

87.06%

12.94%

2006

100%

11.23%

22.10%

36.62%

10.56%

47.17%

20.73%

67.91%

19.68%

87.58%

12.42%

2007

100%

11.95%

22.86%

37.39%

10.49%

47.88%

20.53%

68.41%

19.40%

87.81%

12.19%

2008

100%

10.06%

20.19%

34.95%

11.03%

45.98%

21.71%

67.69%

20.39%

88.08%

11.92%

2009

100%

7.94%

17.21%

32.18%

11.59%

43.77%

22.96%

66.74%

21.38%

88.12%

11.88%

2010

100%

9.24%

18.87%

33.78%

11.38%

45.17%

22.38%

67.55%

20.71%

88.26%

11.74%

2011

100%

8.86%

18.70%

33.89%

11.50%

45.39%

22.43%

67.82%

20.63%

88.45%

11.55%

2012

100%

11.25%

21.86%

36.84%

11.03%

47.87%

21.39%

69.25%

19.64%

88.90%

11.10%

2013

100%

9.03%

19.04%

34.42%

11.45%

45.87%

22.23%

68.10%

20.41%

88.51%

11.49%

2014

100%

10.16%

20.58%

35.96%

11.25%

47.21%

21.70%

68.91%

19.82%

88.73%

11.27%

Year

Total

Top 0.1%

Top 1%

Top 5%

Between 5% & 10%

Top 10%

Between 10% & 25%

Top 25%

Between 25% & 50%

Top 50%

Bottom 50%

Table 6. Total Income Tax Shares, 1980–2014 (percent of federal income tax paid by each group)

Source: Internal Revenue Service.

1980

100%

19.05%

36.84%

12.44%

49.28%

23.74%

73.02%

19.93%

92.95%

7.05%

1981

100%

17.58%

35.06%

12.90%

47.96%

24.33%

72.29%

20.26%

92.55%

7.45%

1982

100%

19.03%

36.13%

12.45%

48.59%

23.91%

72.50%

20.15%

92.65%

7.35%

1983

100%

20.32%

37.26%

12.44%

49.71%

23.39%

73.10%

19.73%

92.83%

7.17%

1984

100%

21.12%

37.98%

12.58%

50.56%

22.92%

73.49%

19.16%

92.65%

7.35%

1985

100%

21.81%

38.78%

12.67%

51.46%

22.60%

74.06%

18.77%

92.83%

7.17%

1986

100%

25.75%

42.57%

12.12%

54.69%

21.33%

76.02%

17.52%

93.54%

6.46%

The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line not strictly comparable

1987

100%

24.81%

43.26%

12.35%

55.61%

21.31%

76.92%

17.02%

93.93%

6.07%

1988

100%

27.58%

45.62%

11.66%

57.28%

20.57%

77.84%

16.44%

94.28%

5.72%

1989

100%

25.24%

43.94%

11.85%

55.78%

21.44%

77.22%

16.94%

94.17%

5.83%

1990

100%

25.13%

43.64%

11.73%

55.36%

21.66%

77.02%

17.16%

94.19%

5.81%

1991

100%

24.82%

43.38%

12.45%

55.82%

21.46%

77.29%

17.23%

94.52%

5.48%

1992

100%

27.54%

45.88%

12.12%

58.01%

20.47%

78.48%

16.46%

94.94%

5.06%

1993

100%

29.01%

47.36%

11.88%

59.24%

20.03%

79.27%

15.92%

95.19%

4.81%

1994

100%

28.86%

47.52%

11.93%

59.45%

20.10%

79.55%

15.68%

95.23%

4.77%

1995

100%

30.26%

48.91%

11.84%

60.75%

19.62%

80.36%

15.03%

95.39%

4.61%

1996

100%

32.31%

50.97%

11.54%

62.51%

18.80%

81.32%

14.36%

95.68%

4.32%

1997

100%

33.17%

51.87%

11.33%

63.20%

18.47%

81.67%

14.05%

95.72%

4.28%

1998

100%

34.75%

53.84%

11.20%

65.04%

17.65%

82.69%

13.10%

95.79%

4.21%

1999

100%

36.18%

55.45%

11.00%

66.45%

17.09%

83.54%

12.46%

96.00%

4.00%

2000

100%

37.42%

56.47%

10.86%

67.33%

16.68%

84.01%

12.08%

96.09%

3.91%

The IRS changed methodology, so data above and below this line not strictly comparable

2001

100%

15.68%

33.22%

52.24%

11.44%

63.68%

17.88%

81.56%

13.54%

95.10%

4.90%

2002

100%

15.09%

33.09%

52.86%

11.77%

64.63%

18.04%

82.67%

13.12%

95.79%

4.21%

2003

100%

15.37%

33.69%

53.54%

11.35%

64.89%

17.87%

82.76%

13.17%

95.93%

4.07%

2004

100%

17.12%

36.28%

56.35%

10.96%

67.30%

16.52%

83.82%

12.31%

96.13%

3.87%

2005

100%

18.91%

38.78%

58.93%

10.52%

69.46%

15.61%

85.07%

11.35%

96.41%

3.59%

2006

100%

19.24%

39.36%

59.49%

10.59%

70.08%

15.41%

85.49%

11.10%

96.59%

3.41%

2007

100%

19.84%

39.81%

59.90%

10.51%

70.41%

15.30%

85.71%

10.93%

96.64%

3.36%

2008

100%

18.20%

37.51%

58.06%

11.14%

69.20%

16.37%

85.57%

11.33%

96.90%

3.10%

2009

100%

16.91%

36.34%

58.17%

11.72%

69.89%

16.85%

86.74%

10.80%

97.54%

2.46%

2010

100%

17.88%

37.38%

59.07%

11.55%

70.62%

16.49%

87.11%

10.53%

97.64%

2.36%

2011

100%

16.14%

35.06%

56.49%

11.77%

68.26%

17.36%

85.62%

11.50%

97.11%

2.89%

2012

100%

18.60%

38.09%

58.95%